Remortgaging Explained

- 5 days ago

- 11 min read

Updated: 4 days ago

Find out how remortgaging works, when to switch, and whether a new deal or a product transfer saves you more in 2026.

Quick Answer

Remortgaging means switching your mortgage to a new deal, usually when your current fixed or tracker rate ends, to avoid your lender's standard variable rate. In 2026 you can move to a new lender or stay put with a product transfer. The right choice depends on the rates, the fees, and whether your circumstances have changed.

Reviewed by Ben Stephenson, FCA authorised (FRN 496907) · 25+ years' experience · 4.9★ on Google. Updated: 16 June 2026.

Who this guide is for

Best for homeowners coming to the end of a fixed or tracker deal, anyone stuck on a standard variable rate, and those wanting to change their rate, term or repayment type, who want to understand how remortgaging works and whether to switch lender or stay put in 2026.

Key points

Remortgage when your fixed or tracker rate ends.

A product transfer stays with your lender.

Avoid drifting onto the standard variable rate.

Table of contents

What is remortgaging, and when should you do it?

Remortgaging is the process of switching your existing mortgage to a new deal, either with a new lender or your current one. Most people remortgage when their fixed or tracker rate is ending, to avoid slipping onto the lender's standard variable rate, which is usually a lot higher. Others do it to change their term, switch repayment type, or simply find a better rate.

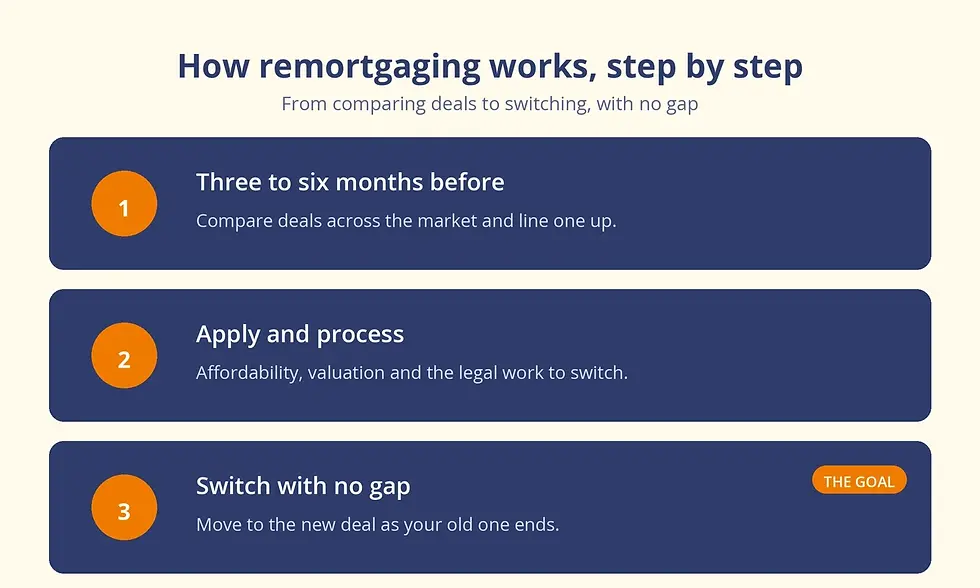

Timing is the key. Lenders typically let you line up a new deal up to six months before your current one ends, and a broker can hold a rate while you wait, so you are ready to switch the day your deal expires rather than drifting onto the expensive default. If your fixed rate is expiring soon, starting early is almost always the right move.

It is not only about the end of a deal. If you are trapped on an uncompetitive rate, have built up equity, or your circumstances have changed, remortgaging can open better options. The Bank of England's base-rate moves feed through to mortgage pricing, so the best time to act is often before your current deal lapses, not after.

Remortgage or product transfer?

When your deal ends you have two main routes. A product transfer means taking a new rate from your existing lender, with minimal paperwork and usually no new affordability check or valuation. A full remortgage means moving to a new lender, which involves an application, a valuation and legal work, but opens up the whole market and often better rates.

Neither is automatically better. A product transfer is fast and simple, ideal if your circumstances have not changed and your lender's rate is competitive. A remortgage takes longer but can save more, especially if you want to borrow more, change the term, or your current lender's deal is poor. Our guides on whether to product transfer or remortgage and comparing the two weigh it up.

Product transfer | Remortgage to a new lender |

Stay with your current lender | Move to a new lender |

Little paperwork, usually no valuation | Application, valuation and legal work |

No new affordability check | Full affordability assessment |

Quick, but only your lender's deals | Slower, but the whole market |

Because the right answer depends on the numbers, it pays to compare remortgage deals across lenders against your current lender's transfer offer. A specialist broker can run both side by side, fees included, so you see the true cost of each.

How does it work, and what does it cost?

A remortgage runs much like your original mortgage application, just usually smoother. After choosing a deal, the lender assesses affordability, instructs a valuation, and the legal work transfers the mortgage from your old lender to the new one, often with free legals on remortgage products. It is best to start around three to six months before your deal ends.

The valuation matters because it sets your loan-to-value, which drives the rate. Sometimes a lender accepts an automated valuation, so you do not need a fresh physical valuation. If you bought recently, there are rules on how soon after buying you can remortgage, often six months with most lenders.

Cost | What to expect |

Arrangement fee | Added to the loan or paid upfront; weigh it against the rate |

Valuation | Often free on remortgage deals, sometimes charged |

Legal fees | Frequently free on remortgage, or a small fixed fee |

Early repayment charge | Applies if you leave your current deal early |

Broker fee | For sourcing and handling the switch |

The headline rate is only part of the cost. A low rate with a high arrangement fee can cost more than a slightly higher rate with no fee, especially on a smaller loan, so always compare the total over the deal period.

A remortgage usually completes in around four to eight weeks, though it can take longer if the valuation is delayed, paperwork is missing, or your situation is more complex. That is another reason starting early matters: it builds in a buffer so you are not forced onto the standard variable rate while you wait. Keep recent payslips or accounts, proof of the property's value, and details of any other borrowing to hand, and respond quickly to the lender and the solicitor. If your income, job or credit has changed since you took out the original mortgage, flag it early rather than late, as it shapes which lenders will offer the best terms and avoids an awkward decline near the finish line. A broker chasing the case on your behalf keeps everything moving and spots problems before they cost you the deal.

Timing it right: when your current deal ends

The window around your deal ending is where the money is won or lost. Most lenders release their retention and remortgage offers a few months ahead, so it is worth knowing what lenders will offer when your fixed rate ends in a few months and lining up the switch. Leaving it to the last minute risks a spell on the standard variable rate. Under the FCA's Consumer Duty, lenders are expected to treat existing borrowers fairly at renewal, but the onus is still on you to act.

Sometimes it makes sense to move before your deal ends, but that usually triggers an early repayment charge. Whether paying it is worth it depends on how much you would save on the new rate versus the charge. In some cases you can remortgage during a fixed term without an early repayment charge, for example with lenders that allow penalty-free switching. How long to lock in next is its own question, covered in our guide on how long to fix for. If you ever feel a lender has treated you unfairly, the Financial Ombudsman Service can consider a complaint.

A typical case

Take an illustrative, composite example. A homeowner's five-year fix is ending on a £180,000 balance. If they did nothing, they would roll onto the lender's standard variable rate and their monthly payment would jump noticeably.

Instead, they start looking four months early, line up a new fixed deal with free legals, and switch on the day the old deal ends, so they never touch the standard variable rate. This is an illustration of the principle, not a quote or a personalised recommendation, and the right move depends on your own deal, balance and circumstances.

Should you fix, track, or stay flexible?

Remortgaging is also a chance to choose the type of rate that suits you now, not just the one you had before. A fixed rate locks your payments for a set period, usually two, five or ten years, giving certainty but charging an early repayment charge if you leave early. A tracker follows the Bank of England base rate plus a margin, so your payments move up or down, often with more freedom to overpay or switch without penalty.

Which is right depends on your priorities and your view of where rates are heading. If certainty and budgeting matter most, a fixed rate usually wins. If you expect rates to fall and value flexibility, a tracker can pay off, though it carries the risk of rises. Some borrowers split the difference, fixing part and tracking part. Our guide on how long to fix for helps you weigh the term, and the standard variable rate is almost never the one to settle on, since it is the expensive default you remortgage to escape.

There is no universally right answer, and the best choice in 2026 may differ from a year ago as the rate outlook shifts. The practical step is to compare the real cost of each option over the period you expect to keep the mortgage, factoring in fees and the chance of moving home, rather than chasing the lowest headline number on its own.

Common situations and life changes

Life rarely stands still, and several situations send people to remortgage. If your house value has dropped, your loan-to-value rises, which narrows options but rarely closes them. Many wonder whether remortgaging extends your term; it can, but it does not have to, and keeping the term the same avoids paying more interest overall.

If you are reaching the end of your mortgage and still owe money, there are routes to deal with it rather than panic. Short-term affordability wobbles sometimes lead people to ask about payment holidays, which can help but have consequences worth understanding first. And major life changes, such as separating or divorcing, often mean remortgaging to move a mortgage into one name. The government-backed Money and Pensions Service offers free, impartial guidance if you want a neutral view of your options.

The thread through all of these is that remortgaging is a tool, not just a rate chase. Used at the right moment it can lower payments, restructure the loan around new circumstances, or buy a little breathing space.

Porting and changing your mortgage type

Remortgaging is not the only way to change your mortgage. If you are moving home, you may be able to port your mortgage, taking your existing rate to the new property and avoiding an early repayment charge. It does not always work, but it is worth checking before assuming you have to start over.

You can also change how the mortgage is structured. Some borrowers switch from repayment to interest-only to lower monthly payments, though lenders apply stricter criteria and want a credible plan to repay the capital. A part-and-part mortgage splits the difference, with some of the balance on repayment and some on interest-only.

Interest-only has its own rules, including a minimum income on many interest-only deals and an acceptable plan to clear the balance at the end of the term. Whether any of these suits you depends on your goals, which is exactly the kind of thing to model with a broker before committing.

Remortgaging later in life

Remortgaging does not stop at a certain age, but the criteria change as you get older. Lenders set maximum ages at the end of the mortgage term, and while many now lend well into retirement, they want to see how the mortgage stays affordable once your income changes. Pension income, investments and other assets can all count, but the picture is assessed more carefully than for a younger borrower.

Interest-only deals are common later in life, where the aim is low monthly payments and the capital is repaid from a pension lump sum, the sale of the property, or other savings. These deals come with a minimum income on many interest-only products and a need to evidence the repayment plan. Retirement interest-only and later-life lending have grown, giving older homeowners more ways to restructure a mortgage than they once had.

If you are approaching the end of a term with a balance left, it is far better to plan a remortgage or switch early than to reach the end with no arrangement in place. A broker who understands later-life lending can map the options, from a standard remortgage to specialist products designed for older borrowers, well before time runs short.

Expert tips and common mistakes

Tips

Start three to six months before your deal ends, so you switch the day it expires.

Compare the all-in cost, fees included, not just the headline rate.

Check whether a product transfer beats remortgaging once the fees are counted.

Keep the term the same unless you have a clear reason to extend it.

Common mistakes

Doing nothing and drifting onto the lender's standard variable rate.

Chasing the lowest rate while ignoring a large arrangement fee.

Assuming you must change lender, when a product transfer may be simpler.

Extending the term without realising how much extra interest it adds.

Frequently asked questions

What does remortgaging mean?

Switching your mortgage to a new deal, with a new lender or your current one, usually when your fixed or tracker rate ends. The aim is to avoid the standard variable rate and secure a better deal.

When should I start remortgaging?

Around three to six months before your current deal ends. Lenders let you line up a new rate in advance, so you can switch the day your deal expires rather than slipping onto the standard variable rate.

Is a product transfer better than remortgaging?

It depends. A product transfer is quick and simple with your current lender, while a remortgage opens the whole market and can save more. Compare both, including the fees, before deciding.

Does remortgaging cost money?

There can be an arrangement fee, valuation and legal costs, though many remortgage deals include a free valuation and free legals. If you leave a deal early, an early repayment charge may apply.

Will remortgaging extend my term?

Only if you choose to. You can keep the same end date, which avoids paying more interest overall, or extend the term to lower your monthly payments.

Can I remortgage if my home has fallen in value?

Often yes, though a higher loan-to-value narrows your options and may mean a higher rate. A product transfer with your current lender can be a simpler route in that situation.

Can I remortgage during my fixed term?

Sometimes, but it usually triggers an early repayment charge. Whether it is worth paying depends on how much the new deal saves you against the charge.

More remortgaging guides

Summary

Remortgaging means switching to a new deal when your current rate ends, so you avoid your lender's standard variable rate. You can move to a new lender for the whole market or take a product transfer to stay put, and the right choice turns on the rates, the fees and your circumstances. Start three to six months early, compare the all-in cost, and remortgaging is one of the simplest ways to cut your mortgage costs in 2026.

Updated: 16 June 2026

Written by Ben Stephenson, CeMAP-qualified Mortgage Broker.

Manor Mortgages Direct is FCA authorised, FRN 496907, has 25 years trading, is highly positively reviewed and 4.9 rated on Google, and has helped thousands secure the right mortgage. Bristol-based mortgage brokers, assisting clients nationwide.

Sources

FCA, Mortgages and Home Finance: Conduct of Business sourcebook (MCOB) - https://www.handbook.fca.org.uk/handbook/MCOB/

Bank of England, Bank Rate and monetary policy - https://www.bankofengland.co.uk/monetary-policy/the-interest-rate-bank-rate

Financial Ombudsman Service - https://www.financial-ombudsman.org.uk/

Related guides