How does your Checkmyfile report affect your mortgage application?

- Nov 4, 2025

- 9 min read

Updated: 6 minutes ago

Updated: 4 November 2025

It’s the underlying credit data, not the score, that lenders assess

Key Points:

You’re assessed on your credit data, not your Checkmyfile score

You’re judged on payment history, balances, searches, and public records

You should expect older issues to remain visible for several years

You can check accuracy, request corrections, or add a Notice of Correction

You won’t affect your score with a Decision in Principle, but applications leave a footprint

Your Checkmyfile report can influence your mortgage application, because it brings together what UK credit reference agencies hold about you. Lenders do not use the Checkmyfile score itself, they assess your underlying data and run their own scorecards and affordability tests.

In practice, underwriters pay close attention to payment history, defaults and CCJs, current balances versus limits, electoral‑roll registration, recent hard searches, and any fraud markers. Issues like defaults or CCJs often remain visible for around six years, and hard search footprints usually show for about twelve months.

A Decision in Principle is commonly a soft search that does not affect your score, while a full application is a hard search. If something is inaccurate, you have a right to rectification, or you can add a brief Notice of Correction. Protective fraud registration does not affect your score, but it may trigger extra lender checks.

Written by Ben Stephenson, CeMAP‑qualified Mortgage Broker, and reviewed by Mortgage Experts. Manor Mortgages Direct is FCA authorised, firm reference 496907, in business for nearly 30 years and 4.9‑rated on Google. We have helped thousands successfully secure the right mortgage. We are Bristol based mortgage brokers, and we assist clients nationwide.

Table of contents

What is a Checkmyfile report, and why do brokers ask for it?

Do lenders see your Checkmyfile score or something else entirely?

How long do late payments, defaults, CCJs and insolvency entries matter?

What are financial associations, and should you disassociate?

CIFAS markers and fraud checks, will that derail a mortgage?

How to prepare your report before you apply, a 90‑30‑7 day plan

Case study, a realistic path from “nearly there” to mortgage‑ready

1) What is a Checkmyfile report, and why do brokers ask for it?

Checkmyfile is a multi‑agency presentation of your UK credit data. It collates information each main credit reference agency holds about you, so you and your broker can spot issues early. A broker asks for it because it is faster than juggling three separate reports, and it helps avoid surprises when a lender runs its own checks.

Key point: The report is a mirror of your data, not a guarantee of lending. There is no universal UK credit file and different agencies can hold different snippets. This is why checking across agencies is recommended before you apply.

Tip: catching one small mismatch, for example a missing electoral‑roll entry or an old address link, could save your application from unnecessary manual review. Missing a single clause or marker could cost you your mortgage offer.

2) Do lenders see your Checkmyfile score or something else entirely?

Short answer: lenders do not use the consumer‑facing score you see in Checkmyfile or with any credit app. Lenders use the underlying data and run their own internal scorecards and policy rules, alongside an affordability assessment under the FCA’s responsible lending standards.

What this means for you: focus on clean, accurate data and strong recent conduct. Chasing a particular score number is less useful than eliminating anomalies, correcting errors, and managing balances and payments sensibly.

3) Which parts of the report matter most to underwriters?

Underwriters look at patterns, recency, and severity. Expect attention on:

Payment history: arrears markers, how recent they are, and whether they are isolated or persistent.

Defaults and arrangements: when they were registered, when settled, and if they reflect a one‑off event or ongoing strain.

CCJs: if present, whether satisfied, and how old they are.

Credit utilisation: balances compared with limits, especially on revolving credit.

New credit and searches: a cluster of applications can indicate stress.

Electoral‑roll registration: helps verify identity and stability.

Addresses and links: clean, consistent address history reduces friction.

CIFAS or fraud markers: may trigger manual checks.

Public records and insolvency: IVA, DRO, bankruptcy and discharge dates.

Broker tip: highlight redeeming context. A late payment following a hospital stay, or a temporary arrangement that is now cleared, sets a different risk picture than an ongoing pattern.

4) Soft search versus hard search, what shows and when?

Soft searches are typical at Agreement or Decision in Principle stage. Only you can see them, and they do not affect your score.

Hard searches occur at full application. They are visible to other lenders and may reduce your score slightly for a time. Multiple hard searches close together may amplify the effect.

Practical takeaway: do your checking and fixing before you submit the full application. Space other applications. Let your broker coordinate so you avoid unnecessary footprints.

5) How long do late payments, defaults, CCJs and insolvency entries matter?

While policies vary, the credit‑file visibility of adverse markers often follows these broad patterns:

Marker on your file | How long it usually shows | What underwriters focus on |

Around 6 years | How recent, and whether isolated or a pattern | |

6 years from the default date | Settled and older is far easier than recent or unsatisfied | |

6 years from the judgment date | Satisfied and explained beats outstanding | |

6 years (impact can last longer) | Usually must be discharged; time since matters |

Late payment markers and settled accounts: typically visible for around six years.

Defaults: typically remain for six years from default date, whether paid or not, though “satisfied” looks better than “unsatisfied.”

CCJs: usually show for six years on the public register and on credit files.

IVA and bankruptcy: typically six years on your credit file from the start date. Bankruptcy may also display until discharge if that is later.

Hard searches: other lenders usually see them for about twelve months.

Broker insight: if an adverse event is nearing its six‑year drop‑off, planning the timing of your application can be decisive. Sometimes waiting a few weeks can transform options. If waiting is not practical, the case can still succeed with the right lender and evidence, but expect stricter terms.

6) What are financial associations, and should you disassociate?

A financial association links your file to another person when you share credit, for example a joint loan or joint current account with overdraft. Lenders may look at an associate’s conduct when assessing your risk.

If an association is out of date, request a disassociation with the agencies once joint products are closed.

Merely living together does not create a financial association. It is about joint credit, not shared addresses.

Broker tip: clients who separate often forget to close an old joint account. That lingering link can keep pulling the other person’s history onto your underwriting radar.

If a former financial link is still on your file, our guide on how a partner's bad credit affects your mortgage explains how to limit the damage.

7) CIFAS markers and fraud checks, will that derail a mortgage?

CIFAS Protective Registration does not change your score, but it does flag your identity for extra verification. Lenders may take longer and ask for more documents. If you previously had a non‑protective fraud marker, your broker will explain what that means for timing and lender appetite.

Tip: failing to mention a fraud‑related entry to your broker can cause a late‑stage decline. Disclose early so the case is planned with the right lender pathway and documents.

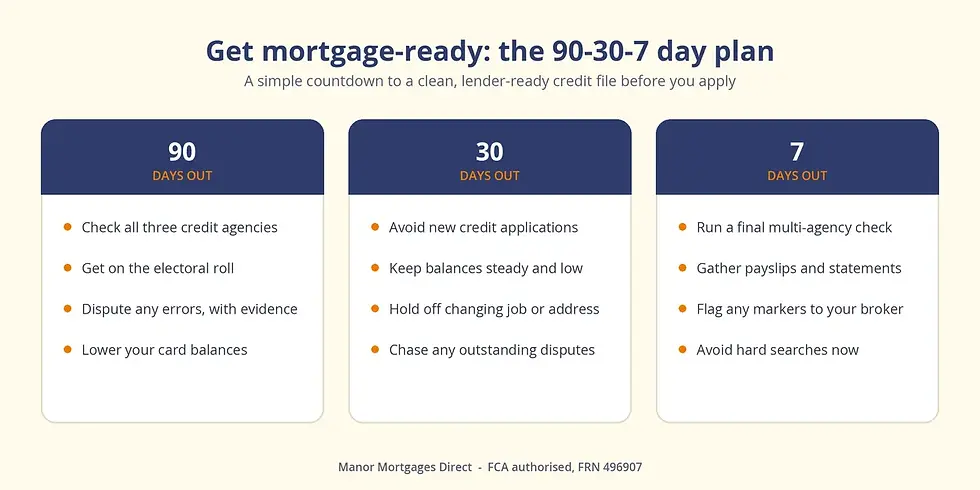

8) How to prepare your report before you apply, a 90‑30‑7 day plan

90 days out

Check all agencies using a multi‑agency report.

Get on the electoral roll at your current address.

Correct errors using each agency’s dispute process, and gather evidence.

Stabilise balances on revolving credit, aim for sensible utilisation.

Avoid new credit unless a broker says it necessary to build history.

30 days out

Address tidy‑up: ensure addresses and dates line up across accounts.

Disassociate from ex‑partners once joint products are closed.

Settle small arrears and make sure the creditor updates reporting.

Consider a Notice of Correction if a material one‑off event explains historic blips. Keep it factual and short.

7 days out

Final sweep: check searches, balances, and that new statements post as expected.

Documents ready: bank statements, payslips, ID, plus any letters that support context, for example a satisfied CCJ certificate.

Tip: progress you can see is motivating. Tick items as you complete them so you keep momentum and reduce stress on offer week.

Fix mistakes early: see common credit report errors and our tips on improving your score, and check how much credit history you really need.

9) What your broker actually does with your report

A good broker will:

Triaging: confirm which issues are historic noise and which are lender‑critical.

Map to criteria: many mainstream and specialist lenders may consider complex files, and some intermediary‑only lenders, for example United Trust Bank, Precise Mortgages, Pepper Money, Foundation Home Loans or Tandem Bank, may review nuanced cases within their risk ranges. This is not a guarantee of acceptance, it is about matching profile to policy.

Affordability sense‑check: ensure the income, commitments and stress rates align with responsible lending requirements.

Packaging: present your case so an underwriter can say “yes” with minimal back‑and‑forth, including the context behind any blips.

Social proof, softly: over many years we have helped thousands of clients with mixed credit profiles. Strong packaging and realistic lender selection often makes the difference.

If an automated system has already declined you, a manual underwriting review is often the way back in.

10) Case study, a realistic path from “nearly there” to mortgage‑ready

Tom and Priya, both employed, came to us after an estate agent asked for a Decision in Principle. Their Checkmyfile showed:

Priya had a satisfied mobile default registered four years ago.

Tom had two recent hard searches from car finance quotes.

Neither was on the electoral roll at the new address after a move.

What we did

Paused any hard DIP, used a soft‑search route first.

Guided Priya to obtain a creditor letter confirming the default was settled and accurate.

Advised Tom to hold off on any further finance while house‑hunting.

Both registered on the electoral roll and updated addresses.

Outcome

Within weeks, their files looked cleaner and the soft DIP aligned with the target loan amount. A full application went ahead with a lender that was comfortable with a single historic, satisfied default and a stable affordability profile. The case completed smoothly because the pack told the story clearly and early.

Takeaway: small tidy‑ups and smart sequencing can turn a borderline file into an acceptable one, without dramatic measures.

11) FAQs

Q1. Does checking my report hurt my mortgage chances?

No. Checking your own report is a soft inquiry and does not affect your score. Focus on accuracy and actioning fixes.

Q2. My score looks fine, do I still need the multi‑agency view?

Yes. There is no single UK file. Lenders may use different agencies, so seeing everything helps prevent a mismatch being discovered mid‑application.

Q3. How do I fix an error quickly?

Raise a dispute with the agency that shows the error and with the creditor that reported it. Under UK GDPR you have a right to rectification where data is inaccurate. Keep evidence ready and be factual.

Q4. Should I add a Notice of Correction?

Use it sparingly and keep to around 200 words and facts only. It can help an underwriter interpret a historic event, but it can add manual steps, so discuss with your broker first.

Q5. I have a satisfied CCJ, how long will it show?

A CCJ typically shows for six years from the judgment. If paid within one calendar month and officially removed, it does not stay on the public register.

Q6. I am in or finishing a DMP or IVA, is a mortgage impossible?

Not necessarily. It depends on recency, conduct, deposit, and overall profile. Some lenders may consider applicants after a period of clean conduct, but terms and options vary and there are no guarantees.

Q7. What if a DIP is a hard search?

Some providers use hard searches even at DIP. Your broker will route you to a soft‑search option where possible and manage timing if a hard search is unavoidable.

Final thoughts and next steps

What matters most is clean data and a credible story. Underwriters read behaviour, timing and context, and they must also meet FCA responsible lending rules on affordability and creditworthiness.

Your Checkmyfile report is the quickest way to see the same raw material they will see, so use it to fix, explain and prepare.

We are expert mortgage advisers with experience in getting mortgages for clients whose Checkmyfile reports are less than perfect.

Get in touch today on 01275 399299

As specialist mortgage brokers we place complex and adverse credit files with lenders every week.

Related Guides