What Bank Statement Red Flags Do Lenders Look For Most?

- Mar 16

- 9 min read

See which bank statement red flags lenders notice most, how much each one really matters, and what you can do before you apply.

Quick Answer

The biggest bank statement red flags are frequent gambling, persistent overdraft use, payday or high-cost credit, returned direct debits, large unexplained deposits, and undisclosed loans. None of these guarantees a decline. Lenders judge patterns over three to six months, and specialist lenders will often accept a one-off blip where the wider picture is strong.

Reviewed by Ben Stephenson, FCA authorised (FRN 496907) · 25+ years’ experience · 4.9★ on Google. Updated: 17 June 2026.

Who Is This Guide For

Best for anyone about to apply for a mortgage who is worried about how their spending looks on paper, from first-time buyers and home movers to the self-employed, especially if there has been gambling, overdraft use, or a missed payment in recent months.

Key Points

Lenders review three to six months of statements

Patterns matter more than one-off transactions

Specialist lenders weigh red flags more flexibly

Table of Contents

Why Do Mortgage Lenders Check Bank Statements?

This guide zeroes in on the warning signs that make underwriters hesitate. If you first want the basics, how many months of statements lenders ask for, what they check, and how to prepare, see our companion guide on whether lenders check your bank statements. Lenders review your statements to confirm three things:

Income consistency

They verify that the income declared on your application matches what actually arrives in your account.

Spending behaviour

Regular spending patterns help lenders understand whether your budget appears sustainable.

Undisclosed commitments

Bank statements can reveal payments to credit providers that may not appear on a credit report.

According to the Financial Conduct Authority Mortgage Conduct of Business rules, lenders must ensure borrowing is affordable both now and in the future.

Bank statements provide real-world evidence of spending habits beyond credit scores.

Related reading: Can You Improve Your Credit Score Fast Enough Before Applying?

The exact number of months requested varies, three is common for employed applicants and up to six for the self-employed, and we break this down by situation in that companion guide. Whichever window a lender uses, the warning signs below are what tip an application from approve to refer.

Specialist lenders, often used in complex applications, may review statements more carefully but also interpret them with greater flexibility.

The Most Common Bank Statement Red Flags

1. Frequent Gambling Transactions

One of the most commonly discussed concerns involves regular gambling activity. Underwriters may view consistent betting transactions as a potential indicator of financial risk.

The UK Gambling Commission reported that around 22.5 million adults gambled in some form in the past year, though most do so responsibly.

Lenders generally focus on:

Frequency of transactions

Size of deposits

Whether gambling appears habitual

Occasional small transactions may not cause issues, but regular high-value betting may prompt additional scrutiny.

2. Persistent Overdraft Usage

Using an overdraft occasionally is normal. However, living permanently in an overdraft can signal cash-flow pressure.

Underwriters often look for patterns such as:

Remaining overdrawn throughout the month

Reaching the overdraft limit regularly

Increasing overdraft reliance over time

According to Bank of England consumer credit data, millions of UK consumers rely on overdrafts each year, but consistent reliance may affect mortgage affordability assessments.

3. Payday Loans or High-Cost Credit

Payments to payday lenders or high-cost short-term credit providers often attract attention.

Examples include:

Payday loan repayments

Buy-now-pay-later arrears

Short-term credit providers

The FCA previously reported that over 760,000 UK borrowers used payday loans annually before tighter regulations were introduced, highlighting why lenders remain cautious.

Even if the loan has been repaid, recent usage may raise questions.

4. Returned Direct Debits or Missed Payments

Returned payments can indicate financial strain.

Examples include:

Utility bills returned unpaid

Credit card direct debits failing

Loan repayments bouncing

A single event may not be significant, but repeated returned payments may concern underwriters.

5. Large Unexplained Deposits

Mortgage lenders must comply with anti-money laundering regulations, which means unusual deposits often require explanation.

Typical examples include:

Large transfers from unknown sources

Cash deposits

Gifts not declared in the application

If funds form part of a deposit contribution, lenders usually request evidence such as a gift letter.

6. Undisclosed Loans or Credit

Some financial commitments do not always appear on credit reports immediately.

Bank statements can reveal payments to:

Personal lenders

Informal loan arrangements

Debt consolidation providers

If lenders notice undisclosed commitments, they may recalculate affordability.

7. Lifestyle Spending Patterns

Underwriters also examine general spending behaviour.

High regular spending on items such as:

luxury purchases

subscriptions

entertainment

travel

does not necessarily prevent a mortgage.

However, if spending significantly reduces disposable income, affordability calculations may change.

At a glance, here is how to soften the impact of each of the main red flags:

Red flag | How to reduce its impact |

Frequent gambling | Cut back well before applying; lenders want a calmer recent pattern |

Persistent overdraft use | Stay within, or out of, your arranged limit for a few months |

Payday or high-cost credit | Avoid new short-term borrowing in the run-up to your application |

Returned direct debits | Keep enough balance so bills and repayments clear on time |

Large unexplained deposits | Keep evidence of the source, such as a gift letter or sale receipt |

Undisclosed loans | Declare every commitment up front so affordability is calculated correctly |

What Underwriters Actually Look For

Many borrowers assume lenders search for mistakes. In reality, underwriters focus on patterns and sustainability. The red flags later in this guide are simply the patterns that break that sustainability.

Key factors include:

Consistency

Stable spending patterns suggest financial discipline.

Transparency

Transactions matching declared income and expenses reduce questions.

Affordability evidence

Disposable income after expenses must support mortgage repayments.

Underwriters often analyse average monthly spending rather than individual transactions.

“Red Flags” Lenders May Spot Immediately

Certain items tend to stand out during statement reviews.

Common immediate flags include:

Recent payday loan usage

Multiple returned direct debits

Large unexplained deposits

Regular gambling transactions

Persistent overdraft usage

Payments to undisclosed lenders

These may trigger further questions rather than automatic declines.

Myth vs Reality About Bank Statement Checks

Myth: Lenders analyse every single purchase

Reality: Most underwriters focus on patterns rather than individual purchases.

Myth: One gambling transaction means rejection

Reality: Occasional betting activity may not cause problems if finances remain stable.

Myth: Spending habits must be perfect

Reality: Lenders expect normal spending behaviour. They mainly assess affordability and risk.

Policy Exceptions Insight

Mortgage criteria often appear rigid, but exceptions sometimes occur.

Certain lenders may overlook some issues where strong compensating factors exist, such as:

large deposits

high stable income

strong credit history

low loan-to-value ratios

For example, a borrower with occasional gambling transactions but a 30% deposit and strong income stability may still be considered by some specialist lenders.

Intermediary-focused lenders such as Precise Mortgages, Pepper Money, Foundation Home Loans, Tandem Bank, or United Trust Bank sometimes assess complex cases with more flexible underwriting.

Criteria vary significantly, and acceptance is never guaranteed.

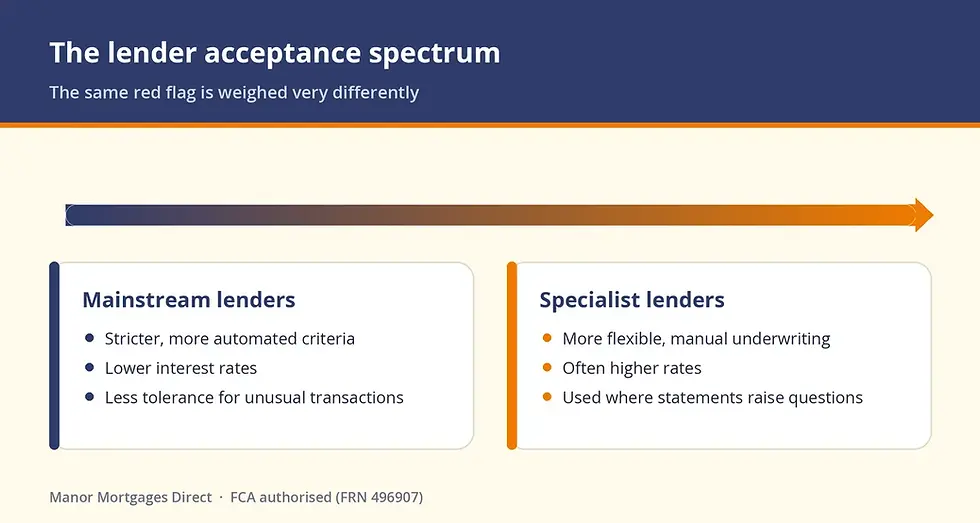

The Lender Acceptance Spectrum

Mortgage lenders generally sit across a risk tolerance spectrum.

Mainstream lenders

Strict criteria

Lower interest rates

Less tolerance for unusual transactions

Specialist lenders

More flexible underwriting

Manual affordability reviews

Often used where bank statements raise questions

Borrowers with unusual financial patterns sometimes find that specialist mortgage routes provide viable solutions. This is often discussed within the broader category of a Specialist Mortgage.

Market Trends: What’s Changed in the Last 12 Months

Mortgage underwriting has evolved in response to economic conditions.

Recent trends include:

Greater scrutiny of spending behaviour

Higher interest rates mean lenders examine affordability more carefully.

More manual underwriting

Some specialist lenders have expanded manual review processes.

Increased regulatory focus

The FCA continues to emphasise responsible lending, particularly regarding consumer vulnerability and affordability checks.

Case Study Example

A borrower approached a broker after a mortgage application was declined due to gambling transactions.

Scenario

Salary £52,000

Deposit 20%

Credit score strong

Several betting transactions per month

A mainstream lender declined the application due to perceived affordability risk.

However, after reviewing the statements, it became clear that:

the betting activity represented less than 2% of monthly income

there were no missed payments or overdraft reliance

disposable income remained strong

A specialist lender reviewed the case manually and offered a mortgage at a slightly higher rate.

This illustrates how context and overall financial stability often matter more than individual transactions.

Expert Tips and Common Mistakes to Avoid

Even small issues can slow down underwriting if explanations are required.

Comparing Different Borrower Types

Different borrowers may face slightly different bank statement scrutiny.

Employed applicants

Usually provide three months of statements confirming salary payments.

Self-employed borrowers

Often need six months of statements, sometimes longer.

Why This Matters in the 2026 Mortgage Market

Mortgage affordability has become more sensitive to spending patterns.

According to Bank of England lending data, mortgage rates increased significantly between 2022 and 2024 before stabilising, which means lenders now stress-test applications more conservatively.

Even small affordability differences can influence lending decisions.

Understanding bank statement checks early can help borrowers avoid unexpected application delays or declines.

Broker Insights: What We See Most Often

From a brokerage perspective, the most common issues are rarely dramatic.

Typical patterns include:

frequent small gambling transactions

regular overdraft use

forgotten buy-now-pay-later agreements

undeclared personal loans

Related reading: Does Using an Overdraft Affect Your Mortgage Application?

Often, these issues can be explained or managed before submitting an application.

This is why many borrowers seek advice before applying, especially when unusual transactions appear on their statements.

FAQs

How many bank statements do mortgage lenders check?

Most lenders request three months of statements, although some applications require up to six months.

Do gambling transactions always cause mortgage rejection?

Not necessarily. Occasional gambling activity may be acceptable if spending remains proportionate and affordability is strong.

Will lenders question large deposits?

Yes. Large or unusual deposits typically require explanation due to anti-money laundering regulations.

Do lenders check everyday spending?

They may review spending patterns to assess affordability, but usually focus on overall trends rather than individual purchases.

Can specialist lenders ignore certain bank statement issues?

Sometimes. Some lenders may consider applications with certain red flags where strong compensating factors exist.

Should I clean up my bank statements before applying?

It can help to avoid new credit, reduce overdraft use, and keep finances stable for several months before applying.

Checklist for Next Steps

If you are planning to apply for a mortgage soon, consider reviewing the following:

Check your last three months of bank statements

Identify any unusual transactions

Prepare explanations for large deposits

Confirm all credit commitments are disclosed

Ensure income matches bank records

Preparing early can help reduce underwriting delays and improve the overall mortgage application experience.

Updated 17 June 2026.

Written by Ben Stephenson, CeMAP-qualified mortgage broker at Manor Mortgages Direct.

Manor Mortgages Direct is FCA authorised (FRN 496907), established for nearly 30 years and rated 4.9★ on Google. Based in Bristol, we help clients across the UK.

More guides on bank statements & affordability

Do lenders question large or unexplained deposits in your account?

Does a returned or missed direct debit affect your mortgage?

Does moving money between your own accounts look bad to a lender?

Do student loan repayments affect your mortgage affordability?

Does paying child maintenance reduce your mortgage borrowing?

Do lenders count child benefit and received maintenance as income?

How do lenders assess affordability if you're paid weekly or four-weekly?