Part and Part Mortgage UK: How It Works, LTV, Income and Exit Strategy

- Jan 29

- 13 min read

Keep payments manageable today, without sleepwalking into a big balance later.

We are FCA authorised (496907) • 25+ years’ experience • Highly Reviewed (4.9★) on Google

Key points:

Split loan: part repayment, part interest-only.

Need credible plan for interest-only balance.

LTV limits are often lower than standard repayment.

Income and outgoings are stress-tested, not property growth.

Review the plan regularly, avoid maturity shocks.

A part and part mortgage (also called a partial interest-only mortgage) is a UK home loan where some of the borrowing is repaid each month (capital plus interest), and the rest is interest-only, meaning the interest-only portion’s capital must be cleared later using an agreed repayment strategy.

It can suit people who want lower contractual monthly payments than a full repayment mortgage, but who still want the discipline of paying down part of the balance. In practice, providers often expect a credible, evidence-backed exit strategy for the interest-only element, and they commonly set stricter limits on loan-to-value (LTV) and may apply higher scrutiny to income and expenditure.

Regulators have tightened standards since the financial crisis, and today affordability assessments should not rely on hoping house prices rise, they look at income, committed outgoings, basic living costs, and potential future rate increases. If your exit plan depends on investments, downsizing, pension lump sums or sale of another asset, you will usually need to show it is realistic and sufficiently funded.

The biggest mistake we see is leaving the exit strategy vague. Planning early, reviewing it regularly, and understanding what happens if circumstances change is what makes part and part work well.

Updated: 29 January 2026

Written by Ben Stephenson, CeMAP-qualified Mortgage Broker, and reviewed by Mortgage Experts.

Manor Mortgages Direct is FCA authorised, FRN 496907, has traded for nearly 30 years, is highly positively reviewed, 4.9 rated on Google, and has helped thousands secure the right mortgage. Bristol-based mortgage brokers, assisting clients nationwide.

Who this guide is for

This guide is designed for you if you are:

Considering a part and part mortgage for affordability, but want to understand the rules around income, LTV and repayment planning first.

Remortgaging from repayment to part and part, for example to reduce monthly commitments while still paying down some capital.

Using a specific future lump sum (pension lump sum, investments, business sale, inheritance expectation, property sale) and want to know what is usually considered “credible”.

Planning around later life (shorter remaining working years), where a full repayment schedule feels too aggressive, but you still want a controlled plan.

Worried about mortgage maturity risk, and want an exit strategy that stands up to scrutiny.

Related guides

Table of contents

What is a part and part mortgage in the UK?

How common are part and part mortgages now?

Why choose part and part, and when does it make sense?

What LTV can you get on a part and part mortgage?

How is income assessed for part and part mortgages?

What counts as a credible exit strategy, and what evidence is used?

Part and part vs repayment, what’s the real cost and risk difference?

Pros and cons you should weigh up

Myth vs reality

Case study: a realistic part and part scenario

Broker insights: what we see most often

FAQs

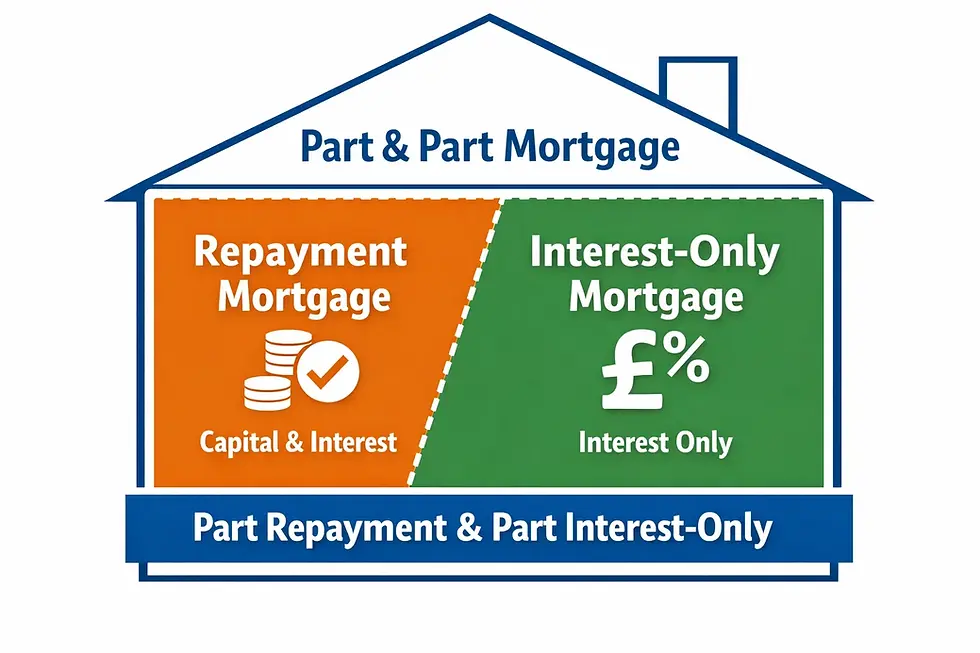

What is a part and part mortgage in the UK?

A part and part mortgage is one mortgage account that is effectively split into two portions:

Repayment portion: you pay interest plus capital, so the balance reduces each month.

Interest-only portion: you pay interest only, so the balance typically stays the same until you repay it using your exit strategy.

The key point is that you still owe the interest-only balance at the end of the term. That is why providers typically want a repayment strategy that is more than “I’ll sort it later”.

A practical way to think about it is this: you are choosing to delay repaying some of the capital, not avoid it. That delay can be useful when affordability is tight, but it increases the importance of planning, evidence, and review.

Is “part and part” the same as having two mortgages?

Usually, no. Part and part is typically one mortgage with two repayment methods applied to different parts of the balance.

That matters because:

affordability is assessed on the overall loan,

the product rate usually applies across the borrowing, and

changing the split later can require a reassessment (and sometimes a full new application).

How common are part and part mortgages now?

Interest-only lending in general is far smaller than it was pre-crisis. The FCA has highlighted that interest-only mortgages were 39% of regulated mortgage sales in 2007, compared with 4.5% in 2024.

Part and part is still a meaningful part of the “interest-only universe”. UK Finance reported 174,000 partial interest-only (part and part) homeowner mortgages outstanding at the end of 2024, and that was 13% fewer than in 2023.

UK Finance also reports the total interest-only stock (including part and part) has reduced 78% in number and 61% in value since 2012. That trend matters because it tells you how cautious the market has become around interest-only risk. Source: UK Finance interest-only mortgages data.

Why choose part and part, and when does it make sense?

Part and part can be sensible when the structure is doing a specific job, and the exit plan is genuinely realistic.

Situations where part and part can work well

Affordability smoothing: You can reduce contractual payments versus full repayment, while still paying down part of the debt.

Time-limited cashflow pressure: For example, childcare years, a temporary income dip, or a planned reduction in working hours later.

Defined future lump sum: Pension lump sum at a known age, a maturing investment, or sale of a secondary asset with clear equity.

Later-life planning: Where the remaining term to retirement makes full repayment payments feel disproportionate, but you still want a structured plan.

The FCA’s wider mortgage work recognises changing borrower needs across life stages, and notes pressures such as retirement adequacy, including its reference to 38% of working-age people being projected to be under-saving for retirement (in its broader discussion about later-life lending and housing wealth).

When part and part is often the wrong tool

“I’ll rely on house price growth.” UK affordability rules explicitly seek to avoid affordability being based on expected price rises. Source: FCA Handbook MCOB 11.6 on responsible lending.

“I’ll just refinance later.” Refinancing is never guaranteed, and depends on future rates, income, age, credit profile, and property value.

“Inheritance will cover it.” Inheritance can happen later than expected, be smaller than expected, or be needed for other reasons.

A useful mindset is: if your exit plan needs everything to go perfectly, it is probably not a plan yet.

What LTV can you get on a part and part mortgage?

LTV (loan-to-value) is the mortgage size divided by the property value, expressed as a percentage.

For part and part, providers often treat LTV as a key risk control because:

part of the balance is not amortising (not reducing), and

the exit strategy may be exposed to market movements (investments, sale proceeds, downsizing values).

Typical LTV patterns we see

While exact limits vary, it is common that:

maximum LTVs are tighter than straightforward repayment mortgages, and

the interest-only portion may be capped as a percentage of the property value or of the total borrowing.

UK Finance’s data shows the market has been reducing higher-LTV interest-only exposure. It reports that the number of interest-only loans at over 75% LTV fell by 25.7% in 2024.

Why your property value assumptions matter

A higher valuation might feel helpful, but you should stress-test your plan. For context, the UK House Price Index shows an average UK house price of £271,188 as of November 2025, with a 2.5% annual increase.

That is not an argument that prices will rise, it is a reminder that values move in both directions, and your exit plan should cope even if the market is less favourable when you need it.

A practical LTV rule-of-thumb

If your strategy is “sale of property” or “downsizing”, a lower LTV generally gives you more margin for:

selling costs,

price fluctuations, and

the cost of your next home.

If your strategy is “investments”, the key is whether the investment is actually on track to meet the target, net of volatility and charges.

How is income assessed for part and part mortgages?

Part and part applications are usually underwritten with two questions in mind:

Can you afford the monthly payments now, and if rates rise?

Is your repayment strategy credible and evidenced for the interest-only part?

Affordability is not meant to be based on property price growth

The FCA’s responsible lending rules state that affordability assessments must not be based on the equity in the property or an expected increase in property prices, and must take account of income net of tax, committed expenditure, and basic living costs.

This is exactly why part and part is not simply “a cheaper way to borrow”. It is still affordability-tested.

Income multiples and loan-to-income limits

Even if your affordability looks fine, there is another constraint that can matter in the UK, loan-to-income (LTI).

The FCA’s guidance reflecting the Financial Policy Committee recommendation is commonly summarised as: lenders should limit lending at 4.5x income (or higher) to no more than 15% of new mortgage lending (per lender).

What this means in practice:

higher loan sizes relative to income can be possible, but are more constrained,

small changes in income evidence (bonuses, overtime, retained profits) can materially affect outcome.

What documents and income types are usually scrutinised

Expect detailed checks on:

basic salary and employment status,

bonuses or commission history and sustainability,

self-employed income, typically using accounts or tax calculations,

regular commitments, credit, childcare, maintenance, and dependent costs.

If you are using part and part because “the payments look lower”, be careful. A common underwriting question

is: are you choosing part and part because it fits a plan, or because a repayment mortgage fails affordability? The second is not automatically a deal-breaker, but it increases scrutiny.

What counts as a credible exit strategy, and what evidence is used?

This is the most important section of the whole guide.

An interest-only balance is only as safe as the plan to repay it.

The FCA definition, and why “credible” is a high bar

The FCA describes interest-only as a mortgage where monthly payments cover only interest, and the borrower needs a method of repaying the capital at the end of the term. It also explicitly describes part and part as paying off some capital, while still having a lump sum to pay at the end.

What repayment strategies are commonly used

In real underwriting, you will usually see strategies such as:

investments and savings (ISAs, general investment accounts, unit trusts or OEICs),

pension lump sum (where accessible and evidenced),

sale of another property (with clear ownership and equity),

downsizing (sale of current property with enough equity to move),

a planned switch to repayment later (with a plausible affordability path).

Important: the FCA’s rules and guidance are designed to discourage “hope” strategies. The FCA’s Mortgage Rule Review discussion paper highlights historic issues where some interest-only loans were taken without a repayment plan, contributing to maturity risk.

Behavioural reality, people often overestimate how “sorted” they are

FCA-commissioned research found:

14% of interest-only holders reported not knowing they needed a separate repayment plan when they took the mortgage,

82% reported being “very” or “fairly” confident they can pay it off, but the research cautions confidence may be overly optimistic,

72% check their plan at least once a year, but 9% never check at all.

That combination, high confidence plus imperfect review habits, is exactly why we encourage clients to create a plan that survives scrutiny.

Evidence, what is usually needed

Evidence varies by strategy, but commonly includes:

latest statements (dated recently),

proof of ownership and whether it is in the applicants’ names,

projections that use sensible assumptions, not best-case scenarios,

pension documentation showing lump sum access and values,

for property sale strategies, clear equity calculations and a realistic downsizing plan.

One missing document can delay underwriting, and one unclear assumption can trigger additional checks. If the property is leasehold, missing one restrictive lease clause can cost you your mortgage offer, or at least delay it while solicitors investigate.

Maturity risk is real, and regulators have focused on engagement

The FCA’s work on existing interest-only mortgages found that nearly 70% of interest-only customers did not engage with their lender, despite efforts to contact them about maturity options.

Separately, UK Finance has highlighted the industry focus on maturities, noting that the number of interest-only loans set to mature by 2027 reduced to 120,000 after falling by 67,000 in 2024. Source: UK Finance interest-only mortgages update (June 2025).

The message for a new borrower considering part and part is simple: build an exit strategy you can evidence, and review it before it becomes urgent.

Part and part vs repayment, what’s the real cost and risk difference?

A part and part mortgage can reduce monthly payments, but it usually increases the total interest paid over time compared with full repayment, because part of the balance is not reducing.

A simple illustrative example (not a quote, rates vary)

Assume a £250,000 mortgage over 25 years at a constant rate (purely for illustration):

Full repayment: you repay capital monthly, the balance falls over time.

Part and part (say 50% interest-only): half the loan balance may remain until the end unless you repay it separately.

Even if the monthly payment looks easier, you are trading:

Lower payments now for a higher planning burden and a future lump sum risk.

In many households, that can be a smart trade, but only when the exit plan is robust.

Risk comparison in plain English

Repayment mortgages concentrate risk in monthly affordability.

Part and part spreads risk across monthly affordability and end-of-term repayment.

If you choose part and part, you are accepting an extra risk category: strategy execution risk.

Pros and cons you should weigh up

Potential benefits

Lower contractual monthly payments than full repayment.

Flexibility, you still reduce part of the balance.

Planning tool, useful around life stages and cashflow.

Overpayment optionality, you may target the interest-only part.

Potential downsides

You still owe a lump sum, the interest-only balance.

Stricter criteria are common, especially on LTV.

Exit strategy can fail, investments underperform, plans change.

Refinance risk, future affordability and criteria may tighten.

Property risk, sale or downsizing assumptions may not hold.

If you take only one lesson from this list, make it this: the “cheap monthly payment” is not the whole cost. The whole cost includes the probability-weighted risk of the exit plan not happening as expected.

Myth vs reality

Myth: “Part and part is basically easier to get”

Reality: It can be harder, because the provider is underwriting both affordability and your repayment strategy.

Myth: “I can rely on house prices going up”

Reality: Responsible lending rules are designed to avoid affordability being based on expected house price

increases.

Myth: “If needed, I’ll just extend the term”

Reality: Term extensions can be possible, but they are not automatic, and later-life affordability can be a limiting factor.

Myth: “Downsizing is always a valid plan”

Reality: Downsizing can be credible, but it must be realistic about future housing needs, sale costs, and local market conditions.

Myth: “If I’m confident, it’s fine”

Reality: FCA research shows high confidence is common, even where plans are not reviewed regularly. Source: FCA interest-only consumer research.

Case study: a realistic part and part scenario

Scenario (illustrative):Priya and Alex are buying a £400,000 home with a £100,000 deposit (75% LTV). They have strong incomes today, but they also have childcare costs and want headroom.

They choose:

£200,000 repayment, to reduce the balance steadily.

£100,000 interest-only, with a defined exit plan.

Exit plan:

£60,000 expected from a pension lump sum at a specific age (supported by pension statements).

£40,000 from a long-term investment plan, with regular contributions, and evidence of current value and funding.

What makes it work:

They treat the investment like a bill, not a hope.

They set an annual calendar reminder to review progress.

They plan a “Plan B” overpayment schedule if the investment underperforms.

What could derail it:

stopping contributions for “just a year”, which becomes three years,

assuming a pension lump sum will be untouched despite other needs,

underestimating how much lifestyle changes near retirement affect affordability.

This is the kind of plan that tends to stand up, because it is specific, evidenced, and reviewed.

Broker insights: what we see most often

1) The split is chosen before the plan exists

If the plan comes second, it is usually weaker. Build the exit strategy first, then decide the split.

2) Overpayments go to the wrong place

Some people overpay but do not clearly target the interest-only portion. If you overpay, be clear what you are trying to reduce, and how the provider allocates overpayments.

3) The plan is “inheritance”

Inheritance can be part of a plan, but it is rarely the strongest single pillar. FCA research notes heavy reliance on inheritance among some interest-only holders.

4) The plan is not revisited after life changes

Job change, children, divorce, illness, business changes, all can alter your plan. Review after any major life event, not just annually.

5) People leave it too late

Regulatory guidance on maturity risk stresses early, frequent communication and realistic options for customers who may not repay in full.

FAQs

1) Is a part and part mortgage the same as an interest-only mortgage?

It is a type of interest-only borrowing, but not fully interest-only. Part of the loan is repaid monthly, and part remains to be repaid later via your strategy. Source: FCA interest-only research definition including part and part.

2) What LTV is usually possible on a part and part mortgage?

It varies, but it is often tighter than full repayment. Market data shows higher-LTV interest-only lending has been reducing over time, reflecting caution around risk. Source: UK Finance interest-only data (over 75% LTV segment).

3) Do I always need evidence of the repayment strategy?

Often, yes. The interest-only element is underwritten on the basis that the repayment plan is credible and realistic, not just stated.

4) Can I switch from part and part to full repayment later?

It may be possible, but usually depends on affordability at the time and the provider’s policy. Do not build your whole plan on the assumption you can switch later, build a plan that works even if you cannot.

5) Is downsizing a credible exit strategy?

It can be, if it is realistic. The more you rely on downsizing, the more important it is to keep LTV conservative and think through where you would actually move to.

6) What happens if I reach the end of term and cannot repay the interest-only balance?

You should speak to your provider early, not at the last minute. FCA guidance on treating customers fairly at maturity focuses on early engagement and considering plausible options for the customer’s circumstances.

7) Is a part and part mortgage good for first-time buyers?

Sometimes, but it is not a default. It can help where affordability is tight, but first-time buyers often have less “Plan B” flexibility. A broker can help sanity-check whether the exit strategy is genuinely credible.

Next steps

If you are considering a part and part mortgage, the fastest way to reduce uncertainty is to build a one-page “exit strategy summary” that answers:

What repays the interest-only balance?

How much is already in place today?

What evidence supports it?

What happens if it underperforms?

When will you review it?

If you want, Manor Mortgages Direct can pressure-test your split, LTV position, and exit strategy in plain English, then advise on whether part and part is genuinely suitable for your situation and future plans.